Mark-to-Market: Where Every Option Finds Its True Value

Ever wonder how options ‘end-of-day marks’ are determined? Behind those ‘closing mark’ prices lies a precise, system-wide process known as mark-to-market, a cornerstone of how OCC safeguards market integrity each day.

But before we examine what it is, let’s clarify what it’s not. It is not the bid price, the offer price, the midpoint, nor the last sale price. Most significantly, it is not a tradable value; actual transactions occur within the bid-ask spread throughout market hours.

What is the Mark-to-Market Process?

The term "mark price" originates from a reporting process known as "mark-to-market." In the context of options, OCC computes these EOD marks using a proprietary 29-point binomial algorithm derived from the Cox-Ross-Rubinstein model. The algorithm takes into account factors such as closing bid/ask markets, implied volatility levels and several others. The objective is to reflect a fair and consistent measure of each contract’s current value for margin and risk purposes.

This critical process helps clearing members maintain adequate collateral when calculating open positions’ daily P&L, margin requirements, and portfolio valuation.

Through this daily mark-to-market process, OCC fulfills its role as a central counterparty and as a Systemically Important Financial Market Utility (SIFMU), ensuring the U.S. options market operates with integrity, transparency, and minimal systemic risk. By providing these risk management services, OCC furthers its mission to promote market stability and integrity.

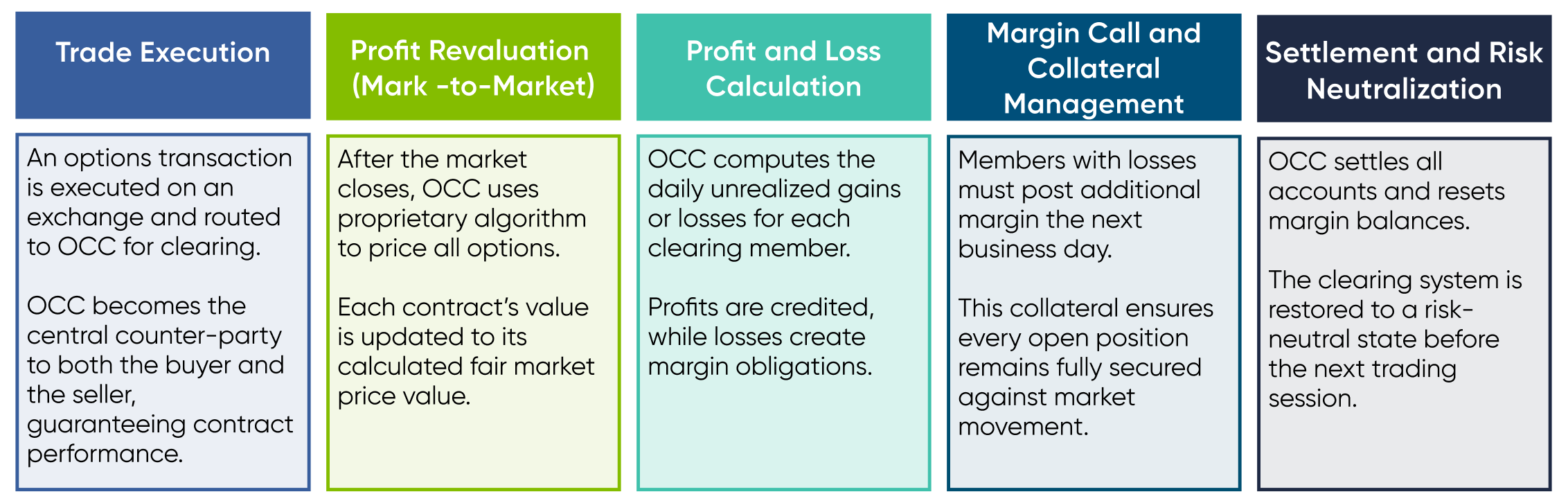

What is OCC's Daily Process?